The Inflation Reduction Act

How the IRA benefits both energy storage manufacturers and customers.

In mid-August, President Biden signed expansive legislation — the Inflation Reduction Act (IRA) — into law. At a high level, the IRA’s goal is to invest in clean energy technologies, lower healthcare costs, create well-paid U.S. manufacturing jobs, and more all while reducing the federal deficit.

For context, the Act is a slimmed down version of the President’s proposed Build Back Better bill that stalled in the U.S. Senate at the end of 2021 due to opposition from West Virginia’s Senator Joe Manchin. Secret negotiations thereafter between Senate majority leader Chuck Schumer and Senator Manchin unexpectedly yielded the IRA agreement at the end of July 2022. It then took just under three weeks from their announcement for the bill to make it to the President’s desk.

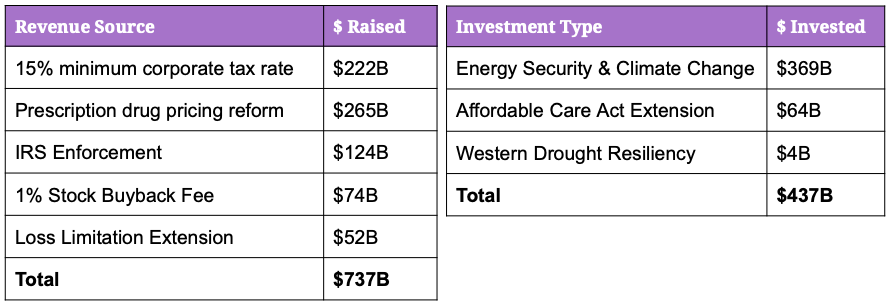

A key feature of the IRA that won Senator Manchin’s vote is its plan to reduce the federal deficit by over $300B. It does this by raising $737B in revenue for the government while investing $437B in energy security and decarbonization, healthcare improvements, and climate change mitigation measures. Here’s a high level breakdown:

The Office of Management and Budget (OMB) claims the above investments put America on track to reduce emissions by 40% by 2030 based on 2005 levels and reduce the social costs of climate change by up to $1.9 trillion.

The IRA has some very attractive incentives for energy storage in particular – both for energy storage manufacturers and customers. Policy is all about the details, so I’ve tried to quote original IRA text where relevant below. Also, note that the Treasury Secretary will be providing more implementation guidance in the coming months to clear up any remaining ambiguities. Lastly, if you need a refresher, there’s a bunch of terminology below that we covered in the last post, Battery Basics.

Incentives for Manufacturing Energy Storage Hardware

The IRA extends and expands the Advanced Energy Project Credit (Section 48C), which is now a tax credit for facilities and equipment that re-quip, expand, or establish U.S.-based manufacturing facilities to support the production or recycling of components for clean technologies and the critical materials used in those technologies.

Starting in 2023, up to $10B in these credits will be awarded through an application process. The text stipulates that $4B of the budget is allocated to “energy communities” to help those who would benefit the most from assistance. An energy community is one that is 1) a brownfield site, or 2) an area that has had significant fossil fuel employment with high current unemployment rate, or 3) is located in or adjacent to a census tract where a coal mine has been retired after 1999 or a coal-fired electric generating unit has been retired.

The base credit rate here is 6% of a qualifying investment, with up to 30% available if the project fulfills two important requirements: the prevailing wage and apprenticeship requirements.

The prevailing wage requirement states that any laborers and mechanics shall be paid wages not less than the “prevailing wage” set by the Secretary of Labor for similar work in the area of the facility. This prevailing wage is required for at least the first 5 years of the project’s operation.

The apprenticeship requirement states that for projects with >4 employees, a certain percentage of labor hours must be completed by qualified apprentices. This percentage starts at 10% (2022) and ratchets up to 15% starting in 2024. However, there is a good faith provision that states that any contractor that attempts to find apprentices, but could not, would be exempted from the requirement.

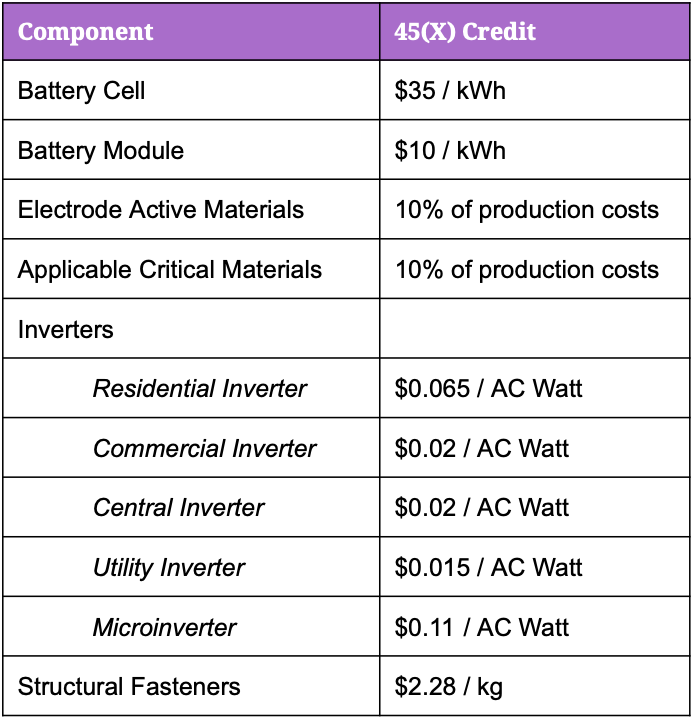

The IRA also introduces a new credit called the Advanced Manufacturing Production Credit (Section 45X), which provides production-volume based tax credits for companies that manufacture eligible energy technology components in the US. These components must be produced by the company and then sold to an “unrelated person.”

There’s a whole list of eligible components, but here are the ones most relevant to energy storage systems:

Of course, there are prescribed definitions for each of the above components! The IRA defines a battery cell as an electrochemical cell with 1 or more positive and negative electrodes, an energy density of not less than 100 Wh/L, and a storage capacity of at least 12 Wh of energy. A battery module is defined as a module that uses “2 or more battery cells, which are configured electrically, in series or parallel, to create voltage or current….”

On the materials side, electrode active materials include cathode and anode materials, anode foil, and “electrochemically active materials, including solvents, additives, and electrolyte salts….” The other applicable materials eligible for a 10% production cost credit include aluminum, cobalt, graphite, lithium, and nickel. For the full list of eligible materials and their required production purity, you can check out Pages 161-163 of the IRA full text.

Inverters, which convert the DC electricity stored in a battery to AC electricity used in a home or on the grid, are defined as so:

Central inverter: for large utility scale systems with capacity >1,000 kW AC

Utility inverter: for large commercial or utility scale systems, with rated output power not less than 600V 3-phase power and between 125 and 1,000 kW AC capacity.

Commercial inverter: for commercial or utility scale applications, with rated output of 208, 480, 600, or 800 volt 3-phase power and has a capacity between 20 and 125 kW AC.

Residential inverter: suitable for residences with rated output of 120 or 240 volt single phase power and <20 kW AC capacity.

Microinverter: more relevant for solar energy, but included for completeness. These are used to connect solar modules, with defined capacity not greater than 650 W AC.

This credit starts a 3-year phase down period starting in 2030, when the benefit is first reduced to 75% of the full value, then to 50% (2031), 25% (2032), and 0% thereafter.

Incentives for Building Energy Storage Projects

The Residential Clean Energy Credit (Section 25D), first introduced in 2006, is a personal income tax credit for direct ownership of eligible hardware. It had started to ramp down from 30% to 26% tax credit in 2022 and would have phased out completely by the end of 2023. Energy storage projects previously were only eligible for this credit if they were paired with an eligible technology, such as solar panels.

The IRA increases this credit back up to 30% and expands the credit to standalone energy storage projects with at least 3 kWh capacity in 2023. The credit starts a 2-year phase down in 2033, when the credit first drops down to 26%, then 22% (2034), and 0% thereafter.

On the commercial/utility-scale side, the existing Energy Investment Tax Credit (ITC) is extended to the end of 2024 and expanded to include standalone energy storage projects with at least 5kWh capacity as well.

The tax credit starts at 6% for eligible investments. Any projects that are <1MW, or fulfill the prevailing wage and apprenticeship requirements, or begin construction within 60 days after the Secretary of the Treasury publishes guidance on those requirements are automatically eligible for the full 30% credit. Otherwise, the project must fulfill the wage and apprenticeship requirements detailed earlier to be eligible for the 30% credit.

The qualified investment for this credit can include the interconnection costs if the project is <5MW, even if the interconnection equipment is owned by the utility — as long as it was paid for by the taxpayer.

There are bonus incentives available beyond the 30% achieved by clearing the prevailing wage and apprenticeship requirements starting in 2023:

Domestic Content (+10%). A project is eligible for this extra incentive if 100% of any steel and iron are from US sources. On top of that, an adjusted percentage of the total costs of manufactured components must also be sourced domestically. That adjusted percentage for energy storage projects starts at 40%, and ratchets up to 55% by 2027. However, taxpayers can apply for an exemption if satisfying this requirement would increase construction costs by 25% or if relevant products are not produced in sufficient quantity or quality in the US. In these cases, those components would be assumed to be 100% domestically produced in the “adjusted percentage” calculation.

Energy Communities (+10%). A project is eligible for this bonus if it’s built in 1) a brownfield site, or 2) an area that has had significant fossil fuel employment with high current unemployment rate, or 3) is located in or adjacent to a census tract where a coal mine has been retired after 1999 or a coal-fired electric generating unit has been retired.

Environmental Justice (+10-20%). A storage project is eligible for this additional bonus only if paired with solar or wind generation located in or servicing a low-income community or Native American lands.

Starting in 2025, the Energy ITC will be replaced by the technology-neutral Clean Electricity Investment Credit (Section 48E). This expands the same tax incentives to any project that generates electricity with a greenhouse gas emissions rate not greater than zero.

These commercial tax credits are set to phase out either in 2032 or when emissions targets are achieved (when the electric power sector achieves 75% lower carbon emissions than 2022 levels). Then, the credit starts a 2-year phase down.

Altogether, the IRA provides some very welcome energy storage incentives for both companies and customers, especially with the expansion of the investment tax credits to standalone energy storage installations. Thanks for reading!